2017-2018 Exhibitions

US plastics machinery shipments fall 7% in Q4 of 2016

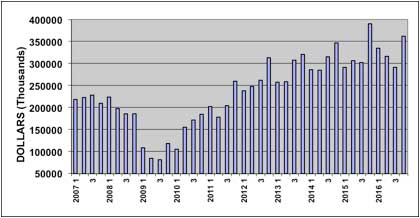

North American shipments of plastics machinery posted a year-over-year decline in Q4 of 2016, according to statistics compiled and reported by the Plastics Industry Association’s (PLASTICS) Committee on Equipment Statistics (CES). This marked the second consecutive quarterly decrease, and it was the first instance of back-to-back quarterly declines since the recovery in the plastics industry began in 2010.

The preliminary estimate for shipments of primary plastics equipment (injection moulding, extrusion, and blow moulding equipment) for reporting companies totaled US$361 million in the fourth quarter. This was 7.4% lower than the robust total of US$390 million from Q4 of 2015, but it was 24.2% higher than the US$291 million from Q3 of 2016. For the entire year, shipments of primary plastics equipment were up 1.2% when compared with the annual total from 2015.

“After rising steadily for six years, shipments of plastics equipment hit a plateau in 2016. The annual total was just high enough to extend the string of annual increases to seven years. The quarterly comparisons will be difficult in the first half of 2017, but the underlying economic fundamentals will gradually improve. If Congress passes corporate tax reform in 2017, then the uptrend in this data may re-emerge later this year,” according to Bill Wood, of Mountaintop Economics & Research, Inc.

PRIMARY PLASTICS EQUIPMENT SHIPMENTS

The shipments value of injection moulding machinery decreased 12.1%, when compared with the total from Q4 of 2015. The shipments value of single-screw extruders decreased 9.2%. The shipments value of twin-screw extruders (which includes both co-rotating and counter-rotating machines) fell by 8.1%, while blow moulding machines increased 9.1% in Q4.

New bookings of auxiliary equipment for reporting companies totalled US$126 million in Q4 of 2016. This represented a slight 0.1% decline from the total from Q4 of 2015, but it was a gain of 5% when compared with the total from Q3 of 2016.

Another indicator of demand for plastics machinery is compiled and reported by the Bureau of Economic Analysis (BEA) as part of the US GDP dataset. According to the BEA, business investment in industrial equipment increased 2.6% (seasonally-adjusted, annualized rate) in Q4 of 2016 when compared with Q4 of 2015. For the year 2016, investment in business equipment rose 2.9%.

"After a modest decline in 2016, overall demand for plastics products in the US will start to rise again in 2017. Our forecast for the economy in 2017 calls for annual, real GDP growth in the range of 3% due primarily to steady improvement in wages and household incomes resulting from stronger employment levels," said Wood.

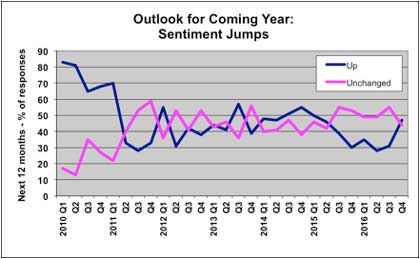

The CES also conducts a quarterly survey of plastics machinery suppliers that asks about expectations for the future. According to the Q4 survey, 91% of respondents expect market conditions to either hold steady or get better during the next year. This is up from 86% in the previous quarter.

The outlook for global market conditions also improved in the third quarter. North America was the region with the strongest expectations for improvement in the coming year. Mexico is expected to be steady-to-better. The outlooks for Asia and Latin America continue to be more optimistic than they were in the previous quarter, while the outlook for Europe weakened modestly.

The respondents to the Q4 survey still expect that medical and packaging are the end-markets that will enjoy the best growth in demand for plastics products and equipment in the coming year. The expectations for automotive demand improved after a sharp dip in the previous quarter. Expectations for all other end-markets call for steady-to-better demand to prevail in 2017.

(PRA)

Copyright (c) 2017 www.plasticsandrubberasia.com. All rights reserved.